Adobe Q4 Update

The CEO Transition, AI Monetization & Why I'm Staying Long

“Earlier today, we announced that I will be transitioning from my role as CEO after over 18 years and 100 earnings calls! Over the coming months I will be working with Frank Calderoni, Adobe’s Lead Director, and the Board of Directors to identify my successor and to ensure a smooth transition. Until then, I will continue to lead Adobe as CEO and will stay on as Chair of the Board to support my successor just as John and Chuck did when I took on this role”

— Shantanu Narayen

Contents

1. CEO Transition

2. FireFly & AI Monetization

3. Financial Performance

4. Innovator’s Dilemma

5. Watch Items

6. Bull Case

CEO Departure

Let’s get this out of the way.

Yes, the CEO of Adobe has left.

The man who took over ‘Adobe Systems’ back in 2007 before the Financial Crisis.

The man who took Adobe through the financial crisis and built one of the most successful enterprise SaaS companies in the world.

Under Narayen's 18 years, Adobe grew from a sub-$1B packaged software company to a $25B+ cloud subscription juggernaut, multiplying the stock price more than sixfold versus ~350% for the S&P 500.

Narayen’s tenure is one of the greatest CEO runs in enterprise software history.

This does sting for long-term Adobe holders!

But, note that Narayen will stay on as Chair of the Board while the company finds his replacement.

I don’t think this departure is necessarily a bad thing. I think it’s natural, and will be a planned, orderly transition.

Narayen is approaching his mid-60’s, and with the world changing so rapidly today, I think it does make sense that he is resigning as CEO.

The board has appointed Lead Director Frank Calderoni to chair a special committee that will evaluate both internal and external candidates…. and the internal bench is deep.

The frontrunner in my view is David Wadhwani, President of Creativity & Productivity. Wadhwani was previously CEO of AppDynamics and actually helped architect the original Creative Cloud shift during his first stint at Adobe.

CNBC has previously reported that Wadhwani was being groomed for the role and former Adobe executive Brad Rencher called him “made in Shantanu’s image”

Wadhwani is currently the executive leading Adobe’s AI transformation and Firefly strategy, which is exactly the skillset needed for this next decade!

Anil Chakravarthy, President of Customer Experience Orchestration, is the other internal contender. He joined from Informatica and oversees the enterprise CXO business (smaller business segment).

Regardless of who gets the appointment, I actually think this is a net positive on a 2-3 year horizon.

Adobe needs a forward-thinking leader who will aggressively push AI-first product innovation and isn’t anchored to legacy business decisions.

Narayen framed the opportunity perfectly on the call:

“Our mission to empower everyone to create represents an even larger opportunity in the AI era.”

Narayen also highlighted that AI-first offering ARR more than tripled YoY, and that Adobe surpassed 850M MAU (monthly active users) across Acrobat, Creative Cloud, Express and Firefly (17% YoY growth).

As always, I would really appreciate if you shared this post and subscribed to ThePrivatePublicInvestor, as I try my hardest each week to give you custom, in-depth analysis on stock investments, market insights and portfolio strategies.

With a subscription to the ThePrivatePublicInvestor, you will receive insight into my personal portfolio, along with each position I own and the related weighting, along with my personal watchlist, custom templates for valuation and modeling (coming soon), additional in-depth analysis on my portfolio holdings, decision-making investment guides, and the personal chat feature for the community.

As this channel grows, paid subscriptions will start to be incorporated, so subscribe early and stay subscribed to receive ‘founding member’ pricing and exclusive benefits.

With that, enjoy this piece and let me know if you have any questions!

Firefly Growth Ramping

Let’s talk about the AI monetization story because this is where the thesis gets hot.

Firefly ARR was $250M+ in Q1, with subscription/credit pack ARR growing 75% QoQ. Generative credit consumption also grew 45%+ QoQ, with video-generative actions surging 8x YoY.

Creative freemium MAU crossed 80M, up 50% YoY, which is a direct feeder in Adobe’s paid conversion funnel.

This is an intentional strategy for conversion.

The monetization architecture/strategy is smart.

First, users get a base amount of generative credits included in their subscription.

Once they exceed that limit, they buy credit packs or upgrade plans.

—> This drives higher ARPU without requiring new seat additions, which is exactly the model I highlighted in my original deep dive.

Even if just 15-20% of Creative Cloud users exceed base AI usage and spend an incremental $10-15/month, that’s hundreds of millions in high-margin revenue!

And remember, Adobe isn’t directly competing with the new, innovative AI models to realize this growth within their existing customer base.

Adobe’s partnerships with Runway (video AI), OpenAI (Sora integration in Firefly Studio), and Google (Gemini models) create a model-agnostic platform, so, if someone builds a better model, it still runs inside Adobe’s software.

Consequently, Firefly Enterprise new customer acquisition grew 50% YoY, with over 2,500 custom models created via Firefly Foundry since launch.

GenStudio and AEP & Apps ARR each ALSO grew over 30% YoY, and there are 650 customer trials underway for Adobe’s agentic web products (LLM Optimizer, Sites Optimizer, Brand Concierge).

The enterprise AI pipeline is building, and customers are buying in….

Q1 Performance: Beats across the Board

Now let’s dig into the general report.

Total Adobe ARR: $26B+, +11% YoY

Q1 Revenue: $6.4B vs. $6.3B expected — BEAT (+12% YoY reported)

Q1 Non-GAAP EPS: $6.06 vs. $5.86 expected — BEAT (+19% YoY)

RPO: $22.2B+, +13% YoY, which is strong forward visibility!

Operating Cash Flow: ~$3B (+19% YoY), which is a Q1 record apparently!

Non-GAAP Operating Margin: 47%+

That’s a great earnings report if you ask me.

Note: there was some tax noise I noticed in the EPS calcs as well, so stripping those out would have realized even more margin expansion and, thus, a larger EPS beat.

One thing I’d like to note here is the accelerating growth of Adobe, which is highly attractive for a mature enterprise SaaS business like this.

The below table shows that Adobe’s product suite is not becoming less attractive or archaic for business or creative users, but rather augmented from AI and AI model integration.

In more detail:

Subscription revenue across both business segments hit ~$6.2B (+13% YoY)

The Business Professionals & Consumers segment grew to ~$1.8B (+16% YoY)

Creative & Marketing Professionals grew to ~$4.4B (+12% YoY)

Acrobat AI Assistant ARR tripled YoY

Express is now used in 99% of U.S. Fortune 500 companies

Guidance also came in pretty good with revenue of $6.4-6.5B (slightly above Street), non-GAAP EPS of $5.80-5.85 (above consensus of $5.68-5.70).

The Innovator’s Dilemma: Is Adobe Falling into the Trap?

Clayton Christensen’s Innovator’s Dilemma warns that incumbent companies get disrupted when they over-serve high-end customers while ignoring cheaper, good-enough alternatives that eat them from below.

Is Adobe falling into this trap? I’d argue no.

Adobe is doing something most incumbents fail to do, which is investing aggressively in the disruptive technology itself rather than protecting legacy revenue streams. They are also focused on democratizing access to this technology through their model-agnostic strategy.

Firefly, Adobe’e new AI platform for creative workflow, isn’t a defensive product, but rather an all-in-one creative AI studio with a broad portfolio of the industry-leading models, a $250M+ ARR business growing 75% QoQ and a clear future monetization framework.

Also, Adobe markets to everyone. Not just their high-value customers.

The one area where the Innovator’s Dilemma does have relevance in conversation is the Stock business decline.

Management admitted this erosion is “happening faster than planned”.

The traditional stock photography/content licensing business (about $450M ARR) is getting cannibalized by Adobe’s own Firefly tools, free AI alternatives and likely competitors.

This is a self-cannibalization trade-off, but I’d rather have Adobe cannibalize its own revenue than let Midjourney or Figma do it for them.

In case you missed it, here are some of the best investing insights for 2026:

What to Watch Going Forward

Despite the strong numbers this quarter, there are legitimate risks that I am not agnostic to:

CEO Succession Uncertainty: Until a successor is named, there’s lost strategic at a very critical time.

An internal pick like Wadhwani would signal continuity and aggressive AI execution, which I think is the right move, but if this gets prolonged, it could extend uncertainty and a continued decline on the stock price.

Competitor AI Momentum: Figma, MidJourney and Canva are strong competitors in the space and are not slowing down.

Figma, for example, is growing at 40% topline and announcing strategic partnerships, such as with Anthropic, integrating Claude Code for AI-powered workflows.

MidJourney also continues to release newer and newer AI models on its platform, challenging industry incumbents like Adobe to keep up.

Canva, Adobe’s biggest competitor, hit $4B in ARR, growing 35% YoY, with 95% Fortune 500 penetration. Their anticipated H2 2026 IPO will bring additional capital and competitive visibility, encroaching on Adobe’s territory.

The SaaSpocalypse: This is the major reason why Adobe’s stock has taken a gigantic hit the past year. About $300B in software market value was wiped in early February 2026 alone!

$IGV, the iShares SaaS ETF, is down (~25%) the last 6 months.

The entire SaaS sector is getting re-rated to lower multiples based on fears that agentic AI will destroy seat-based licensing models, and anyone will be able to vibe-code their way through custom workflows.

I believe this risk is overblown, but it is yet to be seen with certainty whether these re-ratings are appropriate or justified.

Stock Business Erosion: As mentioned, this headwind is accelerating faster than planned and creates a drag on total ARR growth. But, Firefly is accelerating faster than the decline in this business and could successfully replace the traditional creative software offering going forward.

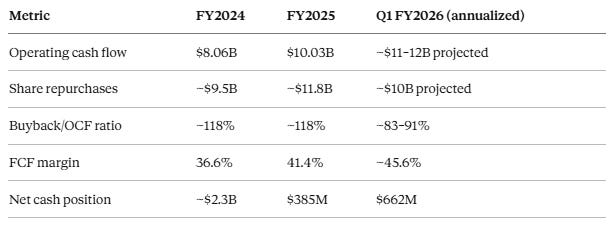

Cash Position & Buybacks: Adobe repurchased roughly 8.1M shares in Q1, leaving ~$3.9B remaining on the $25B authorization. The buyback program was approved in March of 2024, so they’ve burned through almost ALL of that in 2 years.

Adobe’s $25B buyback program will be exhausted by mid-2026, ~2 years ahead of its formal expiration.

Given 7 consecutive buyback program renewals, I would guess they will reinstate this program.

The Semrush acquisition does create a temporary funding pinch, but I don’t think this will be a huge deal considering the operating FCF that Adobe produces.

I’d be on the lookout regarding the size of this buyback program though, as historically, each sequential buyback program has doubled compared to the last, which would infer a $30-40B buyback program this go-around.

A more conservative sizing could acknowledge a tighter balance sheet and growing R&D dollars needed for AI investment.

I’m guessing this announcement will be during the June 2026 earnings call.

I’m Bullish and Staying Long

Despite the SaaS’pocalypse noise, I’m supportive of the bullish thesis on Adobe and think the following are justifiable reasons to invest / stay invested:

Commercial Safety Moat: Firefly is trained exclusively on licensed content with full IP indemnification.

Enterprises will need legal certainty for AI-generated content, and this is a massive differentiator versus Midjourney or other open source tools that can’t offer the same protections.

AI Growth Acceleration: AI-first ARR tripled YoY.

Firefly ARR is growing 75% QoQ, generative credits are growing 45% QoQ and MAU are growing 17% YoY.

The AI business is growing rapidly and faster than anticipated.

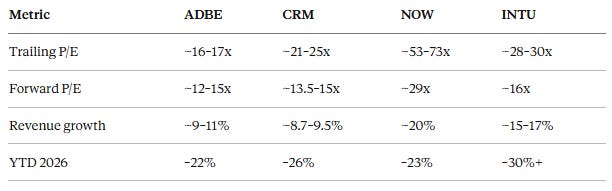

Cheap Valuation: Adobe trades at roughly 15-17x trailing P/E, which is about 63% below its 10-year average.

The forward P/E is lower around 11-14x and the PEG ratio sits at 0.90 (which below 1.0 is traditionally considered undervalued).

For comparison, ServiceNow trades at 53-73x trailing, Intuit at 28-30x and Salesforce at 21-25x.

Adobe is the cheapest large-cap SaaS stock by trailing P/E, despite generating $10B+ in annual operating cash flow and carrying 47% operating margins and an expanding bottom

Wall Street Doesn’t Like It

The analyst community is already cautious.

TD Cowen cut its price target to $325 from $400 CNBC (Hold)

Benzinga HSBC lowered to $302 from $388

Goldman Sachs holds sell rating at $290

Piper Sandler has warned that Adobe sits in software categories “among the least insulated from AI disruption”

UBS reduced to $340 from $375 (Neutral)

Stock Observer Citi trimmed to $315 from $387, expecting an uneventful quarter

Oppenheimer had already downgraded to Perform in January

RBC Capital was among the few bulls, maintaining Outperform with a $430 target.

I like that the Street doesn’t like Adobe now… it only creates opportunity for more upside if the big money decides to jump in later!

Overall

Adobe is accelerating topline growth at 12% for the most recent quarter, with compounding EPS at 19% and trading at a valuation usually reserved for ex-growth businesses.

The math REALLY doesn’t add up unless you believe AI permanently impairs Adobe’s business.

I think these Q1 results suggest the opposite…

Disclaimer: The information provided in this publication is for informational and educational purposes only and does not constitute investment, financial, or other professional advice. ThePrivatePublicInvestor and its authors are not registered investment advisors or broker-dealers. All opinions expressed reflect personal views as of the date published and are subject to change without notice. While efforts are made to ensure accuracy, no guarantee of completeness or reliability is given. Past performance is not indicative of future results. The author may hold positions in securities discussed. Use of this content is at your own risk.

The market reacted poorly to Narayen stepping down, and is rightfully skeptical, however I think in a year or so if Adobe continues producing the type of results they have, and the ceo transition goes well, I’d expect a quick turnaround. Great work as always!