AMD: Mile 6 of the Marathon

Don't confuse the all-time high with the finish line

Stock Popped on Thursday | The Motley Fool")

AMD just printed an all-time high above $340 on Friday without a single piece of company specific news.

Intel blew out Q1 estimates and guided with a story of a severe shortage of CPUs — analysts immediately connected the dots and inferred that if CPU demand is melting up THIS hard, AMD is a HUGE structural winner.

AMD has certainly rallied dramatically from their semi-volatile, no-man’s land malaise since October of last year, but I believe this is only the beginning of AMD’s to-be, most dramatic rally in the lifetime of the company.

I am writing this article in real-time, as I am performing this analysis on the current valuation of AMD.

I didn’t prepare this analysis ahead — rather I am currently working through excel and conducting this analysis in real time.

I want to lay my thoughts out here regarding the current valuation of AMD, and where I realistically see this company’s stock price performing over the remainder of 2026 and forward.

As always, I would really appreciate if you shared this post and subscribed to ThePrivatePublicInvestor, as I try my hardest each week to give you custom, in-depth analysis on stock investments, market insights and portfolio strategies.

With a subscription to the ThePrivatePublicInvestor, you will receive insight into my personal portfolio, along with each position I own and the related weighting, along with my personal watchlist, custom templates for valuation and modeling (coming soon), additional in-depth analysis on my portfolio holdings, decision-making investment guides, and the personal chat feature for the community.

As this channel grows, paid subscriptions will start to be incorporated, so subscribe early and stay subscribed to receive ‘founding member’ pricing and exclusive benefits.

With that, enjoy this piece and let me know if you have any questions!

The Street’s View on the Valuation

The majority of the market’s view on AMD is that it is considerably overvalued when compared with Nvidia, and I would highly disagree with this statement.

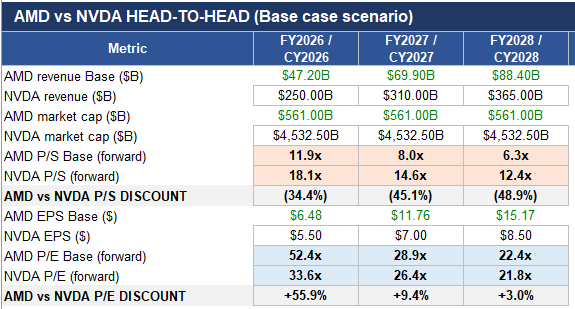

Let’s take a look at the below analysis I ran comparing AMD vs Nvidia on a P/E basis and P/S basis through 2028 based on street consensus.

Based on the current street view, AMD is overvalued on an earnings basis but trading at a discount on a revenue basis.

This makes sense given the current state of AMD’s business.

AMD has lagged Nvidia for the past several years, but has been picking up the pace in compute innovation and breadth.

With the rollout of the MI400 GPUs, the Helios rack-scale architecture, Venice EPYC and the Ryzen AI 400 series all hitting through the back half of 2026, AMD is on the precipice of the most aggressive product cycle in the company's history.

And this will be reflected in their revenue first and flow down to earnings afterwards.

The CPU shortage Intel just exposed will only add fuel to this rally. The Meta $60B / 6 GW deal, the OpenAI 6 GW commitment and Oracle's 50,000 MI450 Helios cluster ALONE imply a step-function in 2026/2027 financials the equity analysts are still scrambling to model.

Bank of America frames it as:

$15-20 billion of revenue per gigawatt of installed AI capacity.

With 12+ gigawatts already locked in across these three deals + implied incremental hyperscaler interest after the Intel earnings = the contractual revenue floor through 2028 is enormous for AMD.

I think we are at mile 6 of the marathon. Still 20 miles to go…

My 5-Scenario Model Build

I built a 5-scenario model — Low / Below Average / Base / Above Average / High — for FY2026, FY2027, and FY2028.