Celsius Q1 Update

I've Watched Celsius for 7 Years. Now I'm Aggressively Buying

For the better part of 7 years I have been watching Celsius Holdings.

It’s the longest I have consistently tracked a name in the market on record.

And I think the time is now to build out a position, especially at the currently discounted valuation.

This Q1, Celsius delivered a double beat, yet the stock sold off.

While the integration of Alani executed near flawlessly, that was overshadowed by the core Celsius brand losing market share to Alani Nu. Domestic dependency on Pepsi is also deepening and near-term margins are suddenly feeling tariff whiplash in aluminum.

The past couple of quarters have fundamentally made investors re-think their thesis and where future growth will be driven from. The core Celsius brand? Alani primarily? Will Rockstar ever get on its feet? Is international growth a primary growth strategy?

I’ll tell you what I think.

Let’s jump in.

As always, I would really appreciate if you shared this post and subscribed to ThePrivatePublicInvestor.

With a subscription to the ThePrivatePublicInvestor, you will receive deeply researched stock deep dives, insight into my personal portfolio, along with each position I own and the related weighting, along with my personal watchlist, custom templates for valuation and modeling, decision-making investment guides, and the personal chat feature for the community.

Subscribe now to receive ‘founding member’ pricing and exclusive benefits before we rollout standard pricing for the rest of the community here on Substack.

With that, enjoy this piece and let me know if you have any questions!

Financials

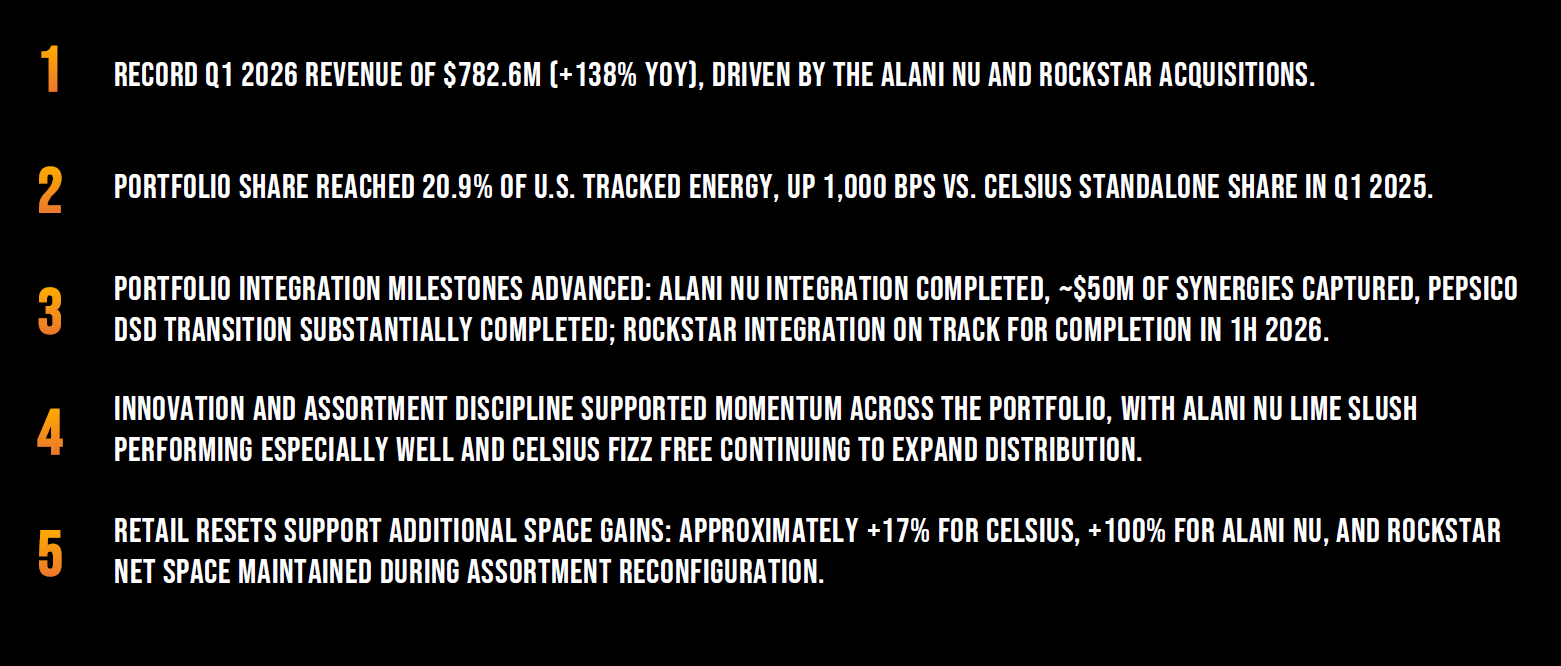

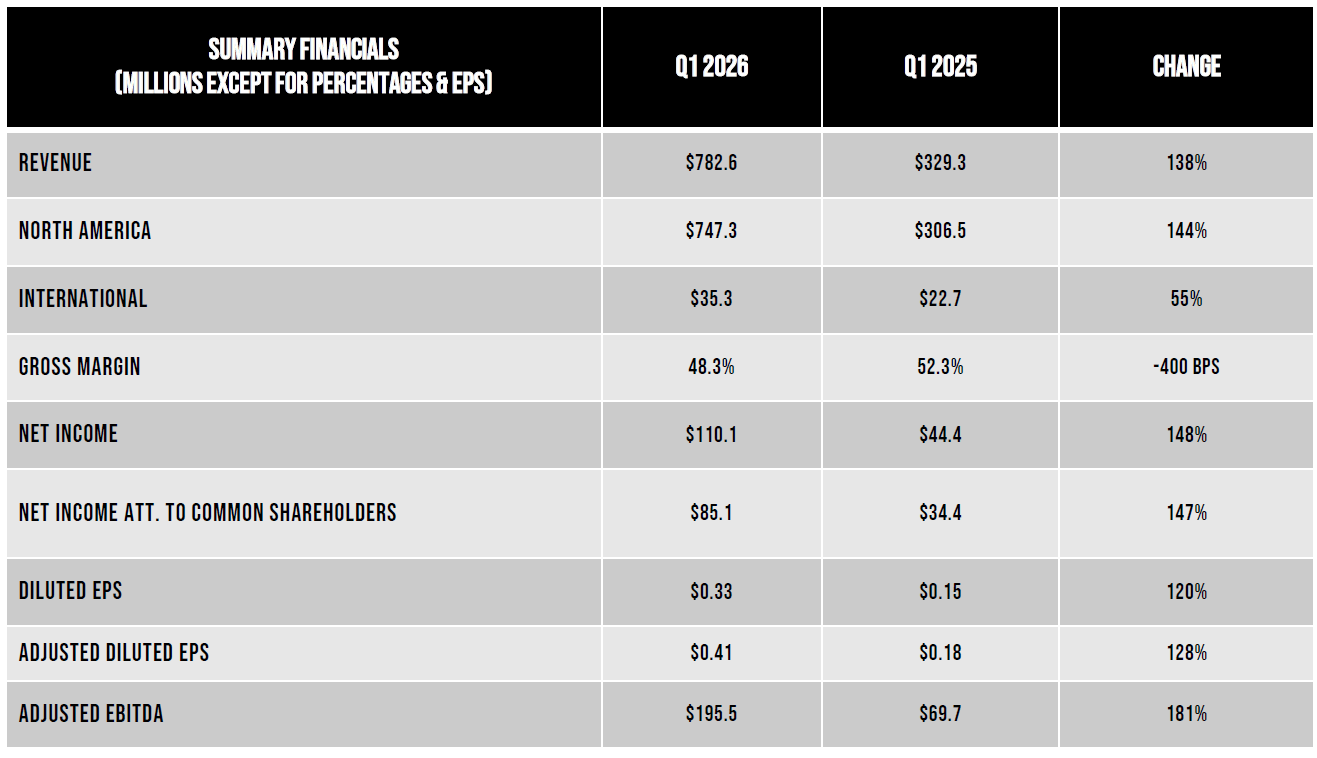

Revenue landed at $782.6M, +138% YoY

Adj. EPS came in at $0.41 vs. the Street at $0.29-0.30

Adj. EBITDA came in at $195.5M, beating consensus by ~28% and the corresponding margin expanded 3.8% to 25.0%, recovering from the Q4 trough at 18.6%

Per normal, no formal full-year 2026 revenue, margin or EPS guidance was issued or updated.

The stock closed +4.45% on earnings day before drifting back toward $30 over the following session(s). That reaction tells me the street is “iffy” on the future roadmap of Celsius, which is exactly where asymmetric trades are born.

Integration

Gross margins suffered this period, down to 48.3% from the low-mid-50’s in Q1-Q2 2025. The primary reasons for this GM compression was increased promotional activity, aluminum price increases and increased freight costs from integration commotion and weather-related drama.

These negative external market dynamics coupled with the Alani/Rockstar acquisition integration have impacted the overall margin profile this past quarter — there’s been a lot of short-term noise with Celsius’ business.

Regarding integration, the Alani Nu synergy target of $50M was captured in full, with management formally calling the integration complete on the call rather than pointing to it as a forward milestone.

In addition, distributor termination cleanup that was hanging over the balance sheet at $264M in December dropped to $40M by quarter-end, with $224M paid out in cash.

Great news!

Jarrod Langhans (CFO) also said the following on the call:

"We do have visibility into the low 50s and beyond with the initiatives and the programs that we have in place... probably as we look at 2026 in particular, Q2 is probably more of a side-step-type activity and then Q3 and Q4, where you're going to see the stair step and then continue on to 2027 with further stair steps."

So the back-to-50’s gross margin plan is structurally there, but the exact timing of this inflection will depend on external market factors — raw material costs (aluminum) and freight costs.

And get this.

Adj. EBITDA reached $195.5M, beating the Street's estimate by nearly 28%.

Gross margin was down during the period but Adj. EBITDA beat by 28% (and no, these weren’t caused by any crazy adjustments).

This means that operating leverage is already being realized post-integration on a cost basis, but revenue hasn’t caught up yet because the Company has been so focused on making the past 6 months of acquisition / integration as smooth as possible.

Now that Celsius has these brands mostly integrated (Rockstar still pending), the flow-through of the topline to the bottom line will inflate EPS meaningfully over the next 24 months.

The Multi-Brand Portfolio

The legacy Celsius brand grew +6% to $348M while Alani Nu came in at $368M, up ~60% PF.

On an LTM basis through Q1 2026, legacy Celsius and Alani Nu are roughly co-equal contributors at approximately $1.25-1.35B each. On a run-rate basis, Alani Nu has already passed legacy Celsius.

Rockstar landed at $66.6M with retail sales down 13% YoY, and Fieldly was clear that 2026 is a stabilization year on that brand rather than a growth year. The team has been focused on Rockstar SKU reconfiguration and resetting the brand maturely, rather than raw growth during integration.

And if you’re unsure about why Celsius acquired Rockstar in the first place, Rockstar essentially gives the portfolio access to convenience channel, gas station shelf and the male traditional energy consumer, which are areas where legacy Celsius and Alani both underpenetrate.

The combined market share of the brands of ~21% sounds great, but the legacy Celsius brand falling about 90 basis points YoY, from 10.8% to 9.9%. Not a great number to see. It’s what the business is built on.

But, the business model is changing, and Celsius is becoming a multi-brand portfolio.

The acquisition of Alani does show management is intelligent about competition and is focused on growing the business into a multi-brand portfolio long-term.

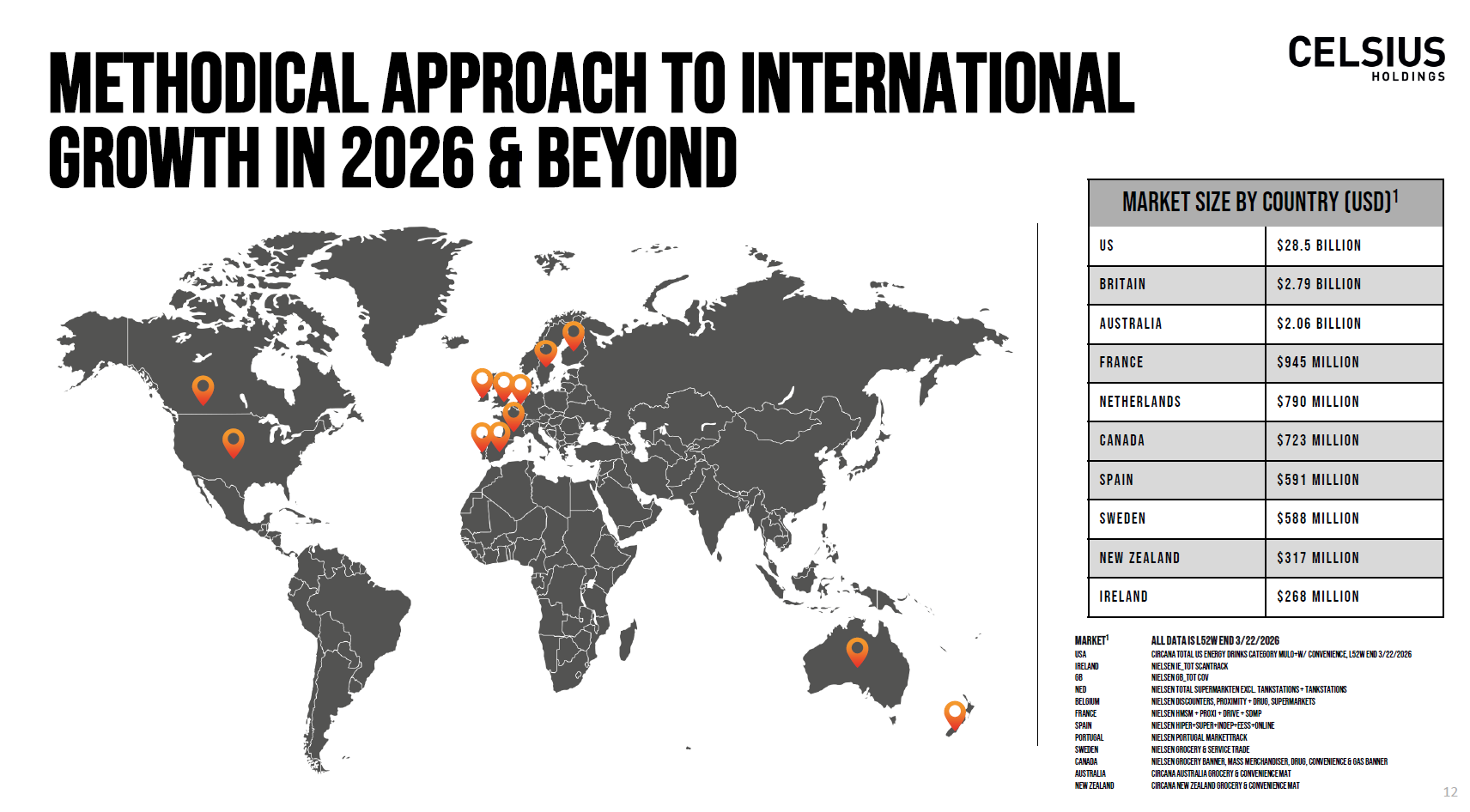

International Growth

International revenue came in at $35.3M, up 55% YoY, with Europe doing the heavy lifting at $25.4M (+36%) and the Asia-Pacific market a smaller base — $7.0M, and growing rapidly YoY at +212%.

That 55% growth looks fantastic, but some investors realized international share of total revenue shrank from 6.9% to 4.5%. This may seem troublesome, but this is simply because the U.S. business is growing that much faster, especially with Alani still on its rapid growth curve.

As of recently in March, Celsius formed an exclusive distribution agreement with Suntory Beverage & Food Spain, with Portugal next on the European footprint under the same partnership.

Fieldly framed the approach as one built on “key markets, strong local partnerships, disciplined launch plans and sustained marketing and distribution support.”

This is literally the SAME EXACT playbook Coke/Monster executed on — find a strong local distributor that already has the route, lean on their reps and skip the cost of building your own international infrastructure from scratch.

It’s a capital-light approach and ramps faster.

For now, I view the international growth plan as set-up to succeed — and just getting started.

What Am I Doing with My Money?

Celsius is currently a top 5 portfolio holding in my portfolio.

I plan for it to be a top 3 position sometime during the next few months, which means I will be continuing to accumulate shares.

This recent earnings report wasn’t great or bad. It was just good.

And good is where asymmetric opportunities are born.

Disclaimer: The information provided in this publication is for informational and educational purposes only and does not constitute investment, financial, or other professional advice. ThePrivatePublicInvestor and its authors are not registered investment advisors or broker-dealers. All opinions expressed reflect personal views as of the date published and are subject to change without notice. While efforts are made to ensure accuracy, no guarantee of completeness or reliability is given. Past performance is not indicative of future results. The author may hold positions in securities discussed. Use of this content is at your own risk.

Just beginning my research on CELH. Will have to check this article out later. Hoping to see prices in the low 20’s.