Celsius Q4 Update

Multi‑Brand Turn & Acquisition Integrations

Energy Drinks Everywhere

You may have noticed that energy drink stocks are still on a tear.

Red Bull sold a record ~14B cans in 2025 (+10.2% YoY), with global sales jumping 8.6% to about $14B+.

Monster had a banner Q4 as well with net sales rising 17.6% to $2.1B, the first time the quarter topped $2B.

The whole category is booming, which makes the backdrop for the Celsius story much more interesting, as the 3rd biggest player now competes in a much fiercer landscape.

Q4 & FY2025 Earnings

Celsius’ Q4 & FY2025 earnings were very strong:

Q4 revenue of $721.6 M (+117% YoY)

FY2025 sales of $2.5B (+86% YoY)

Q4 Adj. EBITDA doubled to $134.1M (+113% YoY)

FY2025 Adj. EBITDA was $619.6M (+142% YoY)

Adj. EPS of $0.26 in Q4 (+86% YoY)

Adj. EPS of $1.34 for FY2025 (+91% YoY)

In short, Celsius exceeded expectations on topline growth, EBITDA and EPS across the board, except for gross margins.

Gross margins were 47.4% in Q4 (down 2.8% YoY) due to integration costs, including Rockstar’s lower-margin mix, tariffs and one-time Pepsi distribution transition fees. However, full year gross margins finished at 50%+ (roughly flat vs. 2024).

Adj. EBITDA margin expanded massively with scale this last report — as Celsius transitions to a multi-brand business, the operating leverage is showing up in the financials.

Management also on the earnings call that as the remaining integration work completes for Alani and Rockstar, margins should rebound to low-50s% in 2026.

The Core Celsius Brand

I drew this up as a major risk in my last post on Celsius.

Investors have been worried about the legacy Celsius brand deteriorating with slower growth YoY.

Based on the latest earnings report, the underlying Celsius brand is still growing.

For Q4, Celsius legacy brand sales were down (8%). This may seem very weak, but U.S. tracked retail sales for the legacy brand actually increased 12.8% during Q4.

The gap between the 8% revenue decline and 12.8% retail growth was attributed to “integration-related timing dynamics” and the sequencing of orders from Pepsi…

Moving Alani Nu into the Pepsi system was a majority contributor in the temporary noise and order misalignments for the legacy brand.

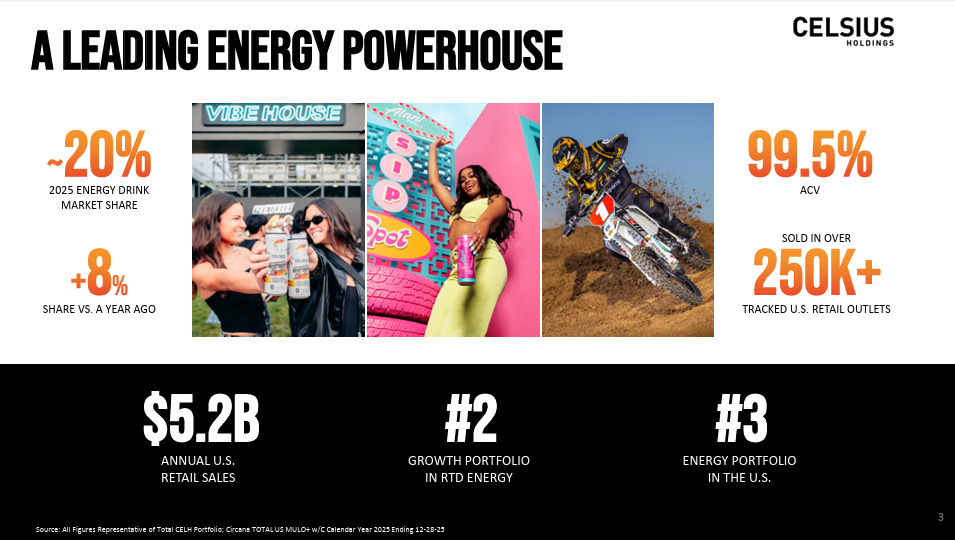

The legacy brand did grow revenue 7.5% for FY2025 and maintained their 10.9% dollar share (essentially market share) of the U.S. energy drink category!

In addition to that, Circana tracker data shows ACV (All Commodity Volume) for the legacy brand has reached nearly 98.5%. Total business ACV reached 99.5%.

—> Essentially, this means that if you walk into almost any store in the U.S. that sells energy drinks, you are very likely to find a Celsius on the shelf.

That is very impressive, but does show us that revenue growth from improved distribution from the legacy brand will be much tougher, as they are already everywhere. Further growth will have to come through more shelf space with existing wholesalers, improved marketing and current customer wallet sell-through.

The Company also guided for a projected 17% increased shelf space for the legacy brand in 2026, which bolsters the foundation for the legacy brand going forward.

Legacy Celsius growth is certainly moderating from its hyper-growth days, but it’s doing so at very high volume and under complex integration conditions, so this feels reasonable and makes me comfortable with the performance.

Alani Nu Integration

This was the main highlight for the earnings report.

Alani Nu added about ~$1B of revenue for 2025, including a record ~$370M in Q4.

YoY retail sales for Alani Nu soared +101% in 2025, driven by aggressive distribution and consumer demand, as the brand has been successfully integrated into Pepsi’s system (not fully).

Alani also released new flavors during the period, which sold out in record time! This flavors include ‘Cherry Bomb’ and ‘Lime Slush’.

One of the craziest stats in the presentation was that the Alani brand surged to 94.2% ACV by the first week of Feb 2026, versus ~87% ACV when Pepsi took over in early Q4. That’s astonishingly successful integration.

—> More ACV means more shelf space and sales velocity.

In addition, Alani Nu's Q4 revenue of $370M (PF growth of 136%), run-rated through 2026 gets you ~$1.5B. Prior to the Alani Nu acquisition, Celsius’ Q1-25 LTM revenue was $1.33B at the time.

This will be a much larger business.

Once Alani becomes full integrated, I think we’ll see extended revenue growth through 2026, along with beneficial synergistic cost realization.

Management noted the Alani transition will be fully complete by end of Q1 2026, which includes supply chain, back office and commercial operations

Rockstar Integration Continues

As a reminder, Rockstar rights for the U.S. was acquired in late August 2025 for $585M. This remains the weakest link of the business.

Rockstar contributed $45M for Q4, and its underlying U.S. sales were down (~10%) in Q4 and (~11%) in FY2025.

Honestly, that decline isn’t surprising to me, as the brand was already in a slump prior to the acquisition, and is now in the process of a distributor handoff.

BUT, at CAGNY, Fieldly described a two-phase strategy for the integration here:

Stabilize by sharpening positioning, improving execution and focusing on the SKU set

Then rebuild by modernizing the brand for today's consumer

—> Management framed this rebuild of the brand as a "handful of years,“ so this transition will be slow

Based on the earnings report, Pepsi is on track to fully transition Rockstar into its system by this summer and project annual revenue post-integration is ~$250M.

We don’t have evidence of the recovery yet, but the integration is proceeding as planned and we’ll be watching to see if the retail declines slow… and eventually show signs of true reversal.

A successful turnaround would allow Celsius to optimize the portfolio, streamline sales teams and leverage Pepsi's network to drive further synergies.

CAGNY 2026 Strategic Foundation (1 week before earnings)

On February 19, leadership presented at the Consumer Analyst Group of New York (CAGNY) conference, revealing key data on portfolio scale and distribution, which actually caused an 8-10% jump in AH trading.

The most impactful data points from CAGNY were distribution-related:

Shelf Space: Expanded by over 25%, with an additional 17% increase forecasted for the legacy Celsius brand and a 100%+ increase for Alani Nu during the upcoming spring reset (when stores refresh their products and Alani supply chain distribution becomes fully integrated), primarily in convenience stores.

Market Reach: The fulsome portfolio now sells through more than 250,000 retail outlets at 99.5% ACV (already talked about this)

Consumer Engagement: 52% of repeat consumers purchase products 5 or more times. This shows brand loyalty and a sticky customer base. The brand is expanding into new occasions as well, with 37% of consumers now drinking Celsius with meals and 33% in social settings.

The Aggregated Portfolio

Celsius is fast becoming a multi-brand player.

As of Q4 2025 the combined Celsius/Alani/Rockstar brands command roughly 20% of the U.S. energy drink category by dollar share (+8% YoY).

This combination of brands is the #3 portfolio behind Red Bull and Monster.

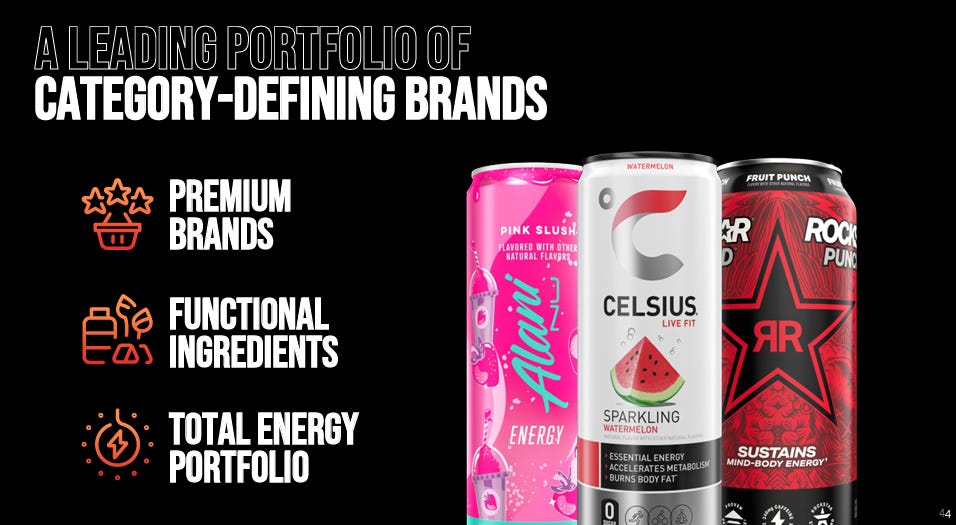

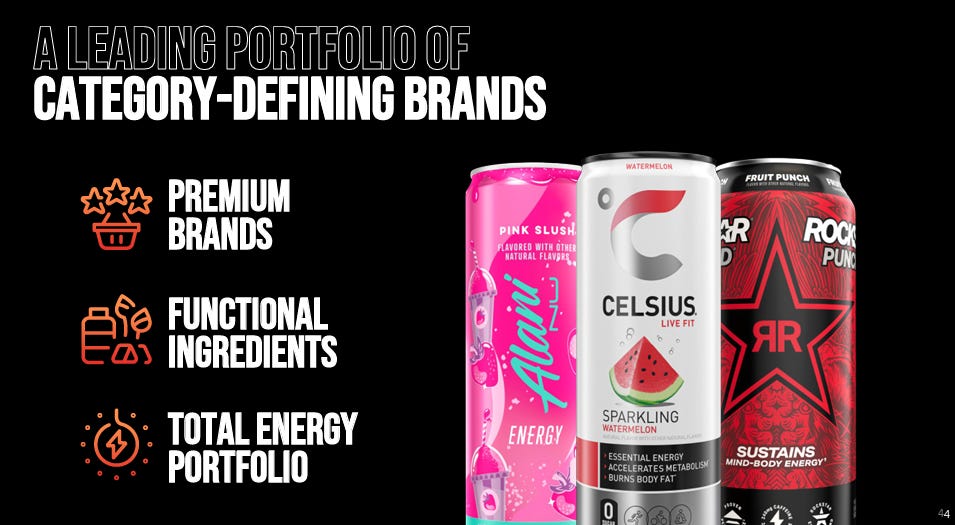

Each brand occupies its own niche as well:

Celsius hits the health/fitness consumers

Alani Nu resonates with females/premium functional space

Rockstar covers the traditional energy segment (maybe a bit more gamer’ish / adventure oriented)

This multi-brand approach allows the Company to go to retailer and say “We have a shelf solution for every energy drink segment.”

This is a major advantage over its competitors Monster and Red Bull.

I also think one of the biggest growth categories within the energy drink market is the zero-sugar segment, and the Celsius (legacy) brand, Alani Nu and Rockstar collectively drove ~33% of the zero-sugar energy sub-category growth in 2025. This should continue through 2026.

Wall Street’s Upgrade Cycle

Post-earnings reactions were overwhelmingly positive, led by BofA’s upgrade from Underperform to Buy, raising their price target to $65.

Broader Analyst Wave:

B. Riley: Raised to $85

JP Morgan: Raised to $77

Needham: Raised to $75

UBS: Raised to $72

Piper Sandler: Raised to $65

Deutsche Bank: Raised to $56

Consensus on Celsius now stands at a Strong Buy with an average price target of $64–68, implying 20–30% upside from where the stock sits today.

What’s Next?

What I’m watching for is:

Margin stabilization: We’ll want to see gross margins tick back up now that integration and distribution shifts are nearly finished. Synergies should be realized as SG&A leverage continues.

Legacy organic growth: I want to see continued, stable growth from the core brand, with no signs of deceleration.

Rockstar’s integration progress: I want to see stabilized Rockstar sales and ACV lift as it comes fully onto Pepsi’s system.

International momentum. This is a huge growth vector, with the Company having almost no exposure abroad. The international business grew ~24% this past year to ~$92.8M, but I want to see this growth accelerate. If Celsius can replicate the U.S. growth playbook abroad, that’s huge long-term upside.

At the end of my last write-up on Celsius, I mentioned:

“I am definitely formulating a plan for selling these shares within the next several months unless organic growth accelerates, integration synergies are successful, distribution is seamless (doesn’t have to be perfect), and the business continues to execute on their core offering.”

This last earnings report certainly got me more comfortable with my current ownership in the business, and I plan on holding these shares for most of 2026.

I would still say I am cautiously optimistic, but this quarter’s execution definitely puts Celsius right on the path we mapped out:

The base Celsius brand stayed strong enough

Alani is integrating on schedule

The setup is laid out for Rockstar to follow

International growth is getting stronger

In addition to this, the current forward P/E of ~28-30x (well below its 5-year median of ~77x) illustrates a reasonable valuation for a company growing revenue 85%+ with a path to mid-50s gross margins with one of the most popular energy drink brands for younger consumers.

While execution risks regarding inventory timing and stabilization remain, the risk/reward profile has shifted meaningfully in favor of shareholders heading into the remainder of 2026.

If the team stays focused and avoids any more negative surprises, the multi-brand thesis story looks alive and well.

Disclaimer: The information provided in this publication is for informational and educational purposes only and does not constitute investment, financial, or other professional advice. ThePrivatePublicInvestor and its authors are not registered investment advisors or broker-dealers. All opinions expressed reflect personal views as of the date published and are subject to change without notice. While efforts are made to ensure accuracy, no guarantee of completeness or reliability is given. Past performance is not indicative of future results. The author may hold positions in securities discussed. Use of this content is at your own risk.

Nice spike this quarter!