Coinbase Deep Dive

The Everything Exchange: Unpacking the Subscription Pivot

I first invested in Bitcoin in 2017.

I transferred $300 into Coinbase and bought $300 of Bitcoin and Ethereum.

I was so excited. I thought I was going to be rich.

But no. One year later, Bitcoin was trading at ~$3,700/coin and Ethereum materially lower. I quit. I concluded that crypto was dumb and just a gambling addition.

But later in 2020 around Covid, Bitcoin exploded again. Then fell. Then exploded again in mid-2023/early-mid 2024.

I wasn’t invested in either of those 2 runs… and it made me very angry! Although, I also realized I was more of a stock investor than a crypto trader.

I started to realize Bitcoin traded in cycles. Lately, I’ve read into the supply/demand patterns and delved into the world of Stablecoins and Tokenized Deposits.

There is actually material utility within crypto and Blockchain technology as a whole.

^That is objective, not an opinion.

I want to be part of this era of crypto/blockchain adoption and believe, apart from outright owning crypto, that Coinbase will be a direct beneficiary.

Executive Summary

Coinbase is no longer a crypto casino (revenue is no longer driven solely on fees from trading volume).

It hasn’t been a casino for a while now, but the market still treats it like one and that’s where the opportunity sits.

Coinbase is down over 60% from its $400+ all-time high last July. The bears have had their days, and frankly, some of their arguments are valid.

Crypto prices are soft. Q4 showed a $667 million GAAP net loss for Coinbase.

Sentiment is ugly and could get worse.

But, while everyone is staring at Bitcoin’s price chart over the past years, Coinbase has been rebuilding itself into a regulated financial infrastructure company; what the internet is calling “a tollbooth” on the rails that institutional money is increasingly forced to travel through.

Assets on the platform have grown 3x over the past three years, with Coinbase now storing over 12% of all crypto globally.

In 2025, total revenue grew 9% to $7.2B despite a soft Q4, with subscription and services hitting $2.8B, up 23% YoY and now 41% of total topline revenue.

Transaction revenue is still $4.1B and very cyclical (floats with trading volume), but the other pieces — USDC, cold storage custody, Coinbase One and derivatives are what actually drive the valuation debate now.

The question for this investment opportunity isn’t whether crypto is going to have another bad quarter. It probably will.

The question is whether Coinbase has built enough durable revenue to survive it, whether it can withstand the multitude of regulatory changes and statues going through government, and whether the long-term structural tailwinds via stablecoins, tokenized assets and regulatory clarity can be materialized and implemented successfully within the economy.

Let’s dive in.

As always, I would really appreciate if you shared this post and subscribed to ThePrivatePublicInvestor, as I try my hardest each week to give you custom, in-depth analysis on stock investments, market insights and portfolio strategies.

With a subscription to the ThePrivatePublicInvestor, you will receive insight into my personal portfolio, along with each position I own and the related weighting, along with my personal watchlist, custom templates for valuation and modeling (coming soon), additional in-depth analysis on my portfolio holdings, decision-making investment guides, and the personal chat feature for the community.

As this channel grows, paid subscriptions will start to be incorporated, so subscribe early and stay subscribed to receive ‘founding member’ pricing and exclusive benefits.

With that, enjoy this piece and let me know if you have any questions!

An Updated View on How Coinbase Makes Money

Before we go further, it's worth grounding ourselves in how this business actually makes money. There are really two buckets of revenue.

In summary:

59% of the business is transaction based

41% of the business is subscription / recurring based

—> If you are already familiar with the business model as of late, feel free to skip this section

Bucket 1: Transaction Revenue ($4.06B in 2025, ~59%)

This is the legacy business, which essentially can be boiled down into fees charged when someone trades crypto on the platform. It breaks down into three pieces:

Consumer trading ($3.32B): This is you or me buying Bitcoin on our phone. Coinbase charges a % spread on each trade, typically around 1-2% for simple trades. This is still the single largest revenue line, but it’s the most volatile. When crypto sentiment dies, this number can fall off a cliff within weeks.

Institutional trading ($480M): Hedge funds, asset managers and other institutional corporations trading in large amounts. The fees are much lower per trade (think 0.05-0.06% of volume) because they are enormous orders.

This line item surged in 2025 due to the Deribit acquisition, which instantly made Coinbase the global leader in crypto options and derivatives. Deribit hit all-time high revenue in Q4.

Other transaction revenue ($253M): These are fees from instant transfers (when you move money to your bank account quickly), Base network transaction fees and payment processing.

Note: Consumer trading margins have been trending down as competition from Robinhood, Kraken and others intensifies — this bucket will always move with crypto sentiment

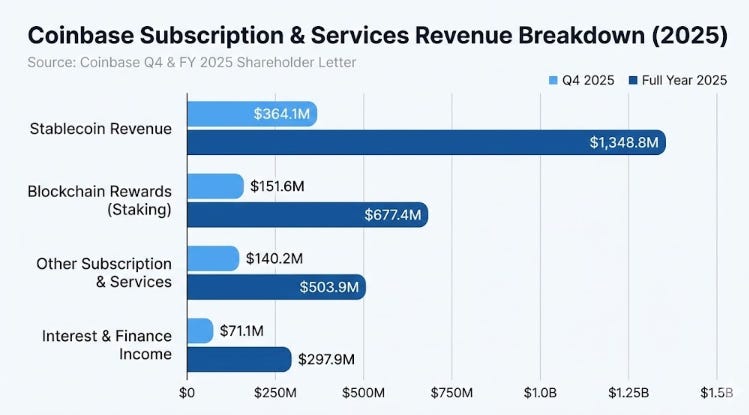

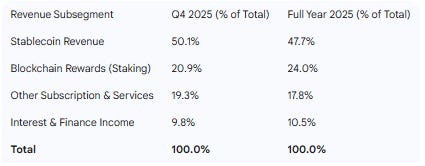

Bucket 2: Subscription & Services Revenue ($2.83B in 2025, ~41%)

This is the new Coinbase — the part the market undervalues, in my opinion. These are revenue streams tied to assets sitting on the platform, not people actively trading. It breaks down into four pieces:

Stablecoin revenue ($1.35B): Through the partnership with Circle (issuer of USDC), Coinbase earns a share of the interest dollars generated by the reserves backing USDC, which are parked in T-bills and cash equivalents (essentially a revenue-sharing agreement).

Think of it like this: every dollar of USDC sitting on Coinbase is effectively a deposit earning Treasury yields, and Coinbase gets a cut of that rate

Blockchain Rewards / Staking ($677M): When you “stake” your Ethereum or Solana through Coinbase, the network pays you rewards for helping validate transactions. Coinbase takes a 25-35% commission on those rewards. (I honestly don’t know the exact nature of how this technically works in the blockchain system).

This revenue is denominated in crypto, so when ETH or SOL prices drop, the dollar value of rewards drops too. The nature of this actually caused a decline recently on their P&L in Q4

Interest and Finance Income ($247M): Interest earned on customer cash balances held at banks + income from Coinbase’s institutional lending business.

Other Subscription & Services ($555M): This comprises of Custodial fees (charged to institutions like BlackRock for storing crypto assets), Coinbase One subscription revenue (paid platform subscribers) and other platform services.

Coinbase holds over 80% of U.S. Bitcoin and Ethereum ETF assets in custody

“Bucket 3”: Other Revenue ($298M in 2025)

This consists of corporate interest income and other miscellaneous items. This is not a driver of the thesis but worth noting, as $11.3B in cash generates meaningful interest income on its own.

The flywheel in the shareholder letter describes the the business pretty well:

Build trust → assets concentrate on Coinbase → users and institutions adopt more products around those assets (staking, borrowing, trading, payments) → revenue grows and is reinvested back into better products and compliance

The Business Model Shift

If you asked me about Coinbase in 2021, I would’ve told you it was a leveraged bet on retail trading crypto euphoria.

Revenue went up 80% when crypto pumped and fell off a cliff when it crashed. That was the old Coinbase!

—> The new Coinbase looks meaningfully different

In 2025, the company generated $7.18B in total revenue, with subscription revenue making up a much larger portion of sales YoY.

This subscription number is 5.5x higher than the 2021 cycle peak!

Inside that subscription bucket, the standout revenue piece is stablecoin revenue, which produced $1.35B in 2025, up 48% YoY. Stablecoin revenue alone now represents ~20% of Coinbase’s total revenue.

Note: In the last period, the ‘Other Subscription & Services’ line item and ‘Interest & Finance Income’ line items have been lumped together for reporting standards, so those 2 bar graphs may have slightly off numbers… but you get the point

The reason this breakdown matters is that it tells you what kind of company Coinbase is becoming versus what it was.

If you model forward several years and assume subscription revenue grows at 15-20% annually while transaction revenue grows steadily or stays flat, you get to a business where the majority of revenue is recurring and asset-based rather than trading-dependent.

Now that is a business that I want to own!

Small caveat: This isn’t true “SaaS” though. If ETH drops 50%, the dollar value of staking rewards, custody fees and even some USDC flows will fall too, even if nobody leaves Coinbase’ platform/ecosystem. I like to think of this as a more stable stream of revenue.

In case you missed it, here are some of the best investing insights for 2026:

Stablecoin Utility is an Asset to Coinbase

If you’re going to own Coinbase, you have to understand stablecoins because this is a big part of where the thesis lives or dies in my eyes.