Earnings Week Volatility

PYPL, AMD, EL & AMZN

Hope everyone enjoyed their Superbowl weekend!

Last week was a BIG week. One of the most action packed weeks I remember since April tariffs in early 2025.

But volatility is fun… I love it.

Usually means there are great opportunities in the market. Great businesses on sale.

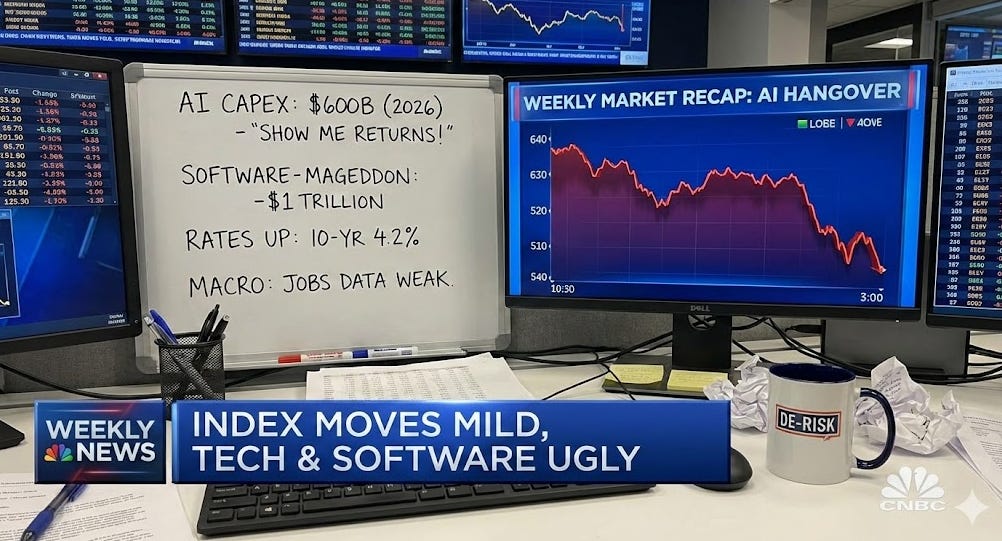

Despite this, Index-level moves weren’t crazy, but under the surface was ugly in software and anything touching tech.

The S&P500 was actually flat YTD this week while some retail investor portfolios were getting smoked, some by 50%+.

Why Markets were Red this Week:

Capex Budgets: Between Google, Amazon and other hyperscalers, investors are looking at ~$600B of planned AI and datacenter Capex spend for 2026. Investors were looking for ROI on historical Capex spend during this earnings season, and it has not shown up credibly thus far. Tbh, I don’t know why investors were expecting it this early. These things take time, especially when it’s a new, innovative technology.

Software Valuations: The S&P ‘Software and Services’ index was down ~8% this past week, wiping out about $1 trillion of market cap value as investors are suddenly price in AI displacement / disruption risk to legacy enterprise SaaS providers such as Intuit, ServiceNow, Adobe, Salesforce, Workday, Hubspot and many more.

Rates: The 10‑year sits around 4.2%, offering an attractive yield for the first time in awhile. Vanguard’s CIO was actually on TV telling people to tilt their capital exposure toward bonds. This will naturally compress multiples investors are willing to pay.

Macro & Policy Noise. Investors are pulling back because new data showed job growth is weaker than expected (hypothetically signaling a cooling economy). This combined with new Federal Reserve chair Kevin Warsh has created a “de-risk” mood in the market amongst investors, with some floating to safer bets.

I do think after this week of hurt, we should see a modest recovery in the market… but that is not certain whatsoever. I can also see the market selling off further. A 5-10% correction in the indices / S&P500 would not surprise me at all.

With that market summary, let’s now jump into this week’s earnings, specifically 4 positions in my portfolio: PYPL, AMD, EL and AMZN

As always, I would really appreciate if you shared this post and subscribed to ThePrivatePublicInvestor, as I try my hardest each week to give you custom, in-depth analysis on stock investments, market insights and portfolio strategies.

With a subscription to the ThePrivatePublicInvestor, you will receive insight into my personal portfolio, along with each position I own and the related weighting, along with my personal watchlist, custom templates for valuation and modeling (coming soon), additional in-depth analysis on my portfolio holdings, decision-making investment guides, and the personal chat feature for the community.

As this channel grows, paid subscriptions will start to be incorporated, so subscribe early and stay subscribed to receive ‘founding member’ pricing and exclusive benefits.

With that, enjoy this piece and let me know if you have any questions!

PayPal Q4 Earnings

PayPal had a pretty poor performance this quarter, and canning Alex Chriss did not help with the stock performance. PayPal announced before the bell on February 3rd, reporting a double miss:

Revenue miss of $8.68M, missing expectations of $8.82

EPS miss of $1.23, missing expectations of $1.29

PayPal also reported lackluster 2026 guidance:

FY2026 Adj. EPS guidance to decline by mid single digits % YoY

Transaction margin dollars to be roughly flat or slightly down

Management also withdrew its prior 2027 long-term outlook and stated the Company will now provide guidance only 1-year at a time due to the pace of change in the industry.

For my portfolio, this report informed me that my thesis was not materializing, and it would likely take awhile before the Company does execute on my envisioned thesis.

The new strategy of the new product roadmap and branded checkout re‑acceleration has been failing, and I think there are better opportunities in the market.

Part of the thesis was also my belief and confidence in Alex Chriss turning around the organization. Since he has been pushed out, I have decided to sell my full position in this stock.

I took a ~35% loss on this position, which is a tough loss. I do believe the rest of my portfolio will make up for this during 2026, and I will still outperform the market.

I did learn a lot with this trade, to be honest:

I didn’t understand the value proposition fully when entering this position, and was not super familiar with the payment processing (FinTech) industry

Can’t make this mistake going forward — know the industry well, the competitive threats and the KPIs a company tracks

There’s also usually a reason for low valuations of a business when the rest of the industry is trading higher; it’s not always disconnect, but rather objective

Do not put too much confidence in management; focus on the numbers, competitive moat and financial performance

Numbers and the moat speak louder than management usually. Even if management is a stellar group of individuals, the business may not be strong and capable of turning around

At the end of the day, PayPal might still work out from here, but it no longer fits what I’m trying to target and build in my portfolio.

There’s too much strategic drift and uncertainty around the core checkout business, and there isn’t enough evidence that the turnaround will materialize.

I’d rather accept the loss, free up my mental bandwidth and redeploy that capital into other names where the growth runway, competitive moat and leadership are all heading positively in the same direction.

Advanced Micro Devices Q4 Earnings

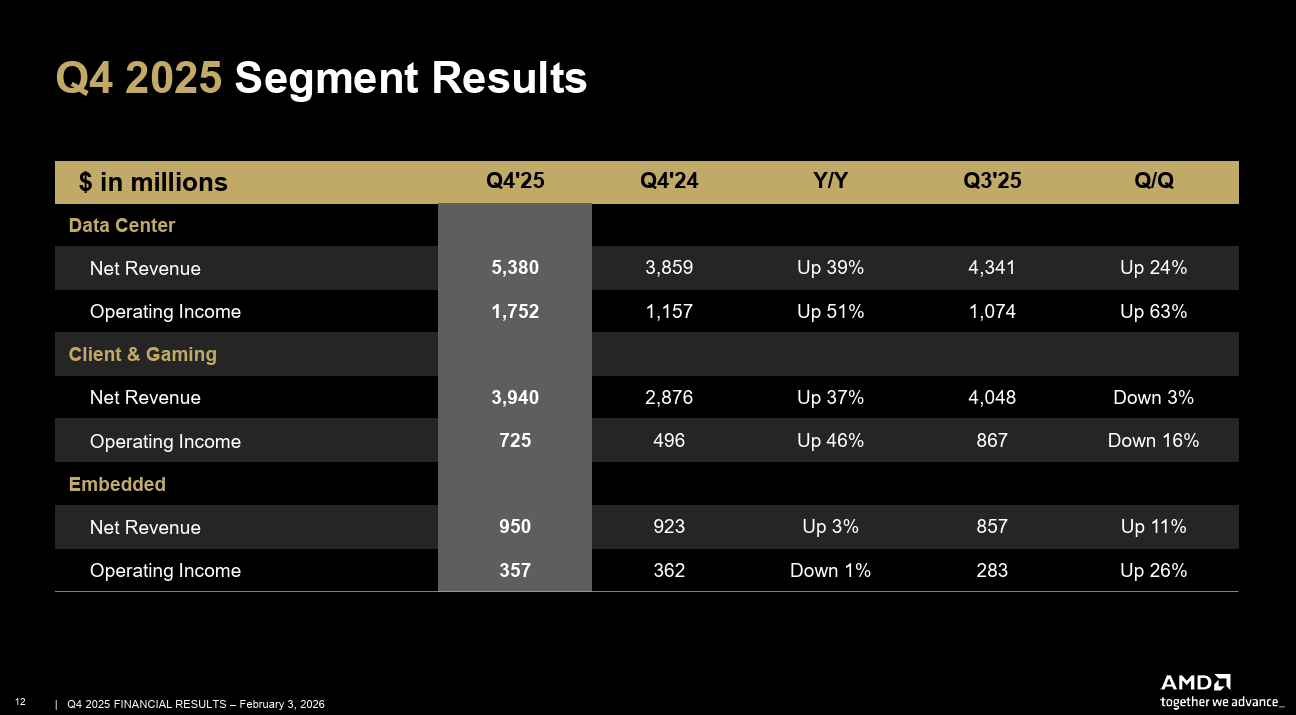

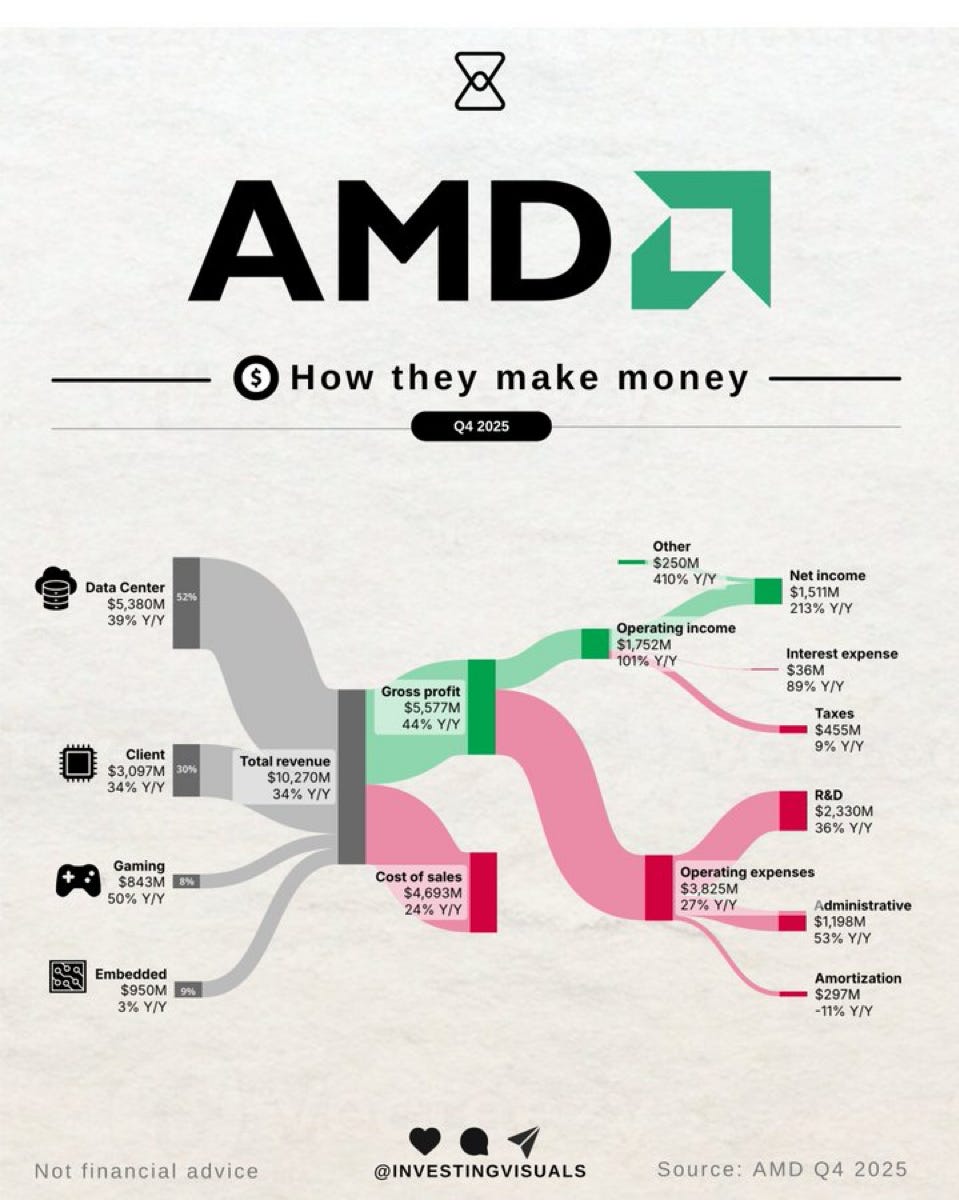

AMD earnings showcased superb performance in Q4 and FY2025.

AMD’s beat on revenue and margins.

Q4 Revenue: $10.3B (+34% YoY)

Data Center Revenue: $5.4B (+39% YoY)

GAAP EPS: $0.92

This ramping revenue growth was driven mainly by EPYC CPU adoption and the GPU portfolio scaling rapidly.

But, the stock got hammered AH because guidance came in slightly below expectations and investors were pricing in nonstop upside.

Wall Street was looking for more near-term AI revenue upside rather than the softer guide that was delivered.

AMD actually experienced their worst single-day decline since 2017, falling over 17%. What do I call that? Stupidity. Dumb. Short-sighted. That’s what I call that.

Remember though: Lisa Su rarely overspeaks

In a post-earnings CNBC interview, she said demand for AI compute has been “accelerating at a pace I would not have imagined” over the last 60-90 days.

Su also signaled:

Real pull-through demand later this year as MI400/MI450 volumes ramp

CPU orders have been strengthening over the last 60+ days

AMD expects data center revenue to grow >60% annually over the next 3–5 years

Although revenue performance was impressive and “technically” beating expectations (despite the stock getting hammered), earnings (EPS) results were lackluster on a GAAP basis, which helped drive the stock down AH.

Analysts and the rest of the market are tied to the financial engineering of margins with GAAP vs NON-GAAP accounting adjustments.

GAAP EPS: $0.92

Non-GAAP EPS: $1.53 (64% uplift purely from accounting adjustments)

Let me bridge this for you below:

Starting Point: $0.92 GAAP EPS

Stock-Based Compensation: +$0.29 (shareholder dilution and non-cash)

Amort of Acquisition Intangibles: +$0.34 (Xilinx/prior acquisitions and non-recurring)

Other Adjustments: ($0.02)

Ending Point: $1.53 Non-GAAP EPS

Let’s look at the full year 2025 adjustments:

Starting Point: $2.65 GAAP Diluted EPS

Stock-Based Compensation: +$1.00 (shareholder dilution, non-cash)

Amortization of Acquisition-Related Intangibles: +$1.38 (Xilinx/prior acquisitions and non-recurring)

Release of Reserves for Uncertain Tax Positions: ($0.52) — one-time IRS benefit from reasonable cause relief for dual consolidated losses which was approved in Q2 2025; this won’t repeat in 2026

Other Items: ($0.34) — miscellaneous items

Ending Point: $4.17 Non-GAAP Diluted EPS

The argument here is that headline beats for Q4 and and full-year 2025 are being manufactured through these adjustments, not through genuine business improvement.

AMD needs to show that the underlying GAAP margins can hold and expand as they scale, rather than relying on adjustments and one-time benefits. The operational momentum is great, but the multiple paid for the business is increasingly being questioned by the market.

But it’s important not to throw the baby (the business) out with the bathwater (the accounting).

The company outlook is still more bullish than ever:

AMD has the stage to showcase their banner year with the rollout of the MI400 series and the Helios architecture, which Lisa mentioned on the earnings call will have no delays.

In addition, AMD’s FCF is legitimate. 2025 FCF hit $5.5B versus $2.4B in 2024; there is definitely some real growth and operational leverage being realized.

The data center segment’s 39% Q4 revenue growth in Q4 is also genuine demand, not “accounting magic” like the margin story.

Lastly, the Company is clearly winning share in high-performance GPUs, continuing to grow their CPU and gaming business and scaling AI inference workloads.

Estée Lauder Q2 2026 Earnings

Estée Lauder reported their Q2 2026 earnings last Thursday (Feb 5th), beating top and bottom line estimates for the quarter.

Quarterly Adj. EPS of $0.89 per share, surpassing estimates of $0.83–$0.84

Quarterly Revenue reached $4.23B (~6% YoY), slightly exceeding expectations of $4.22B

The Company also raised 2026 guidance, but did warn of a $100M tariff hit in the second half of the CY. The overall guidance fell short of analyst estimates.

The guidance triple-miss led to one of the worst performing earnings report reactions for the Company, with the stock tanking ~20% before / during market open.

This was an overreaction, in my opinion, and I think Citigroup agrees, as they upgraded the stock to Buy on Friday (Feb. 6), suggesting they believe the 20% pullback offers an attractive entry point, as the company’s ‘Beauty Reimagined’ strategy continues to improve the underlying fundamentals.

Back to the earnings report:

Organically,

Skincare and fragrance grew ~6%

Haircare grew ~5%

Makeup fell (~1%) (seems to be the problem child)

From a regional standpoint, China performed very well with roughly +13% organic growth, with strong brand contributors to this growth from La Mer, Tom Ford and Le Labo, both online and in travel retail.

Europe/UK/Middle East/Africa grew +2%, while the Americas were flat, which tells me the demand recovery isn’t fully back (but rather in progress).

Overall, the 3 big bullish signals in this report (besides WholeCo revenue and earnings) were:

Double-digit growth in China

Significant operating margin expansion (14.4% vs. 11.5% in prior year)

Accelerated product innovation

China Innovation Center

High growth categories (dermatological beauty and luxury fragrance)

AI and predictive analytics for predicting trends

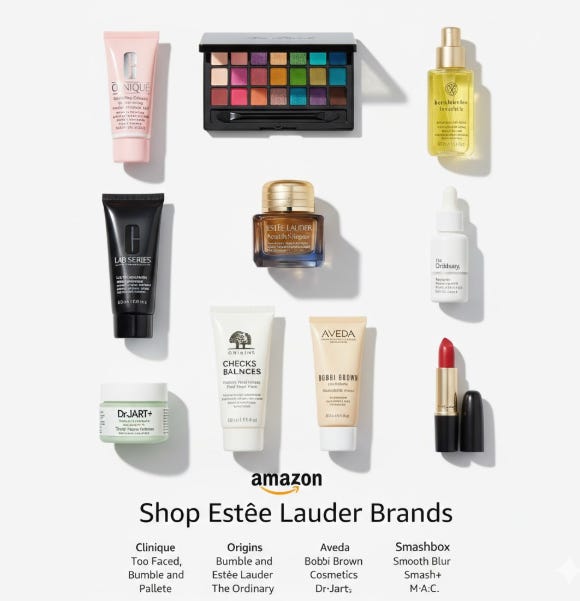

I really liked seeing the increase in online sales, which grew to a record 31% of FY25 sales, driven by more brands rolling onto Amazon and other popular platforms such as TikTok Shop.

Estée Lauder actually first launched on Amazon with the debut of Clinique in March 2024, and since then have introduced more brands to the platform, including Too Faced, Bumble & Bumble, Lab Series, flagship Estée Lauder and several more, with the most recent debut to Amazon being Bobbi Brown, which was released on Amazon last fall in November.

The Company now has 12 brands available on the Amazon Premium Beauty store in the U.S.

Separately, during the earnings call, CEO Stéphane de la Faverie framed remaining FY2026 as the inflection point in the Company turnaround.

He said “With three fiscal years of sales decline and operating margin erosion behind us, we enter fiscal 2026 with signs of momentum and the start of our turnaround, a return to top-line growth… and the pursuit of a solid double‑digit operating margin in the years ahead.”

This is great news and signals to investors the “Kitchen Sink” earnings reports are over, and Estée Lauder is on its way towards profitable growth as the turnaround continues.

I remain bullish on the turnaround, but there are 3 key obstacles the Company must overcome if they are to succeed:

Tariffs and Resulting Margin Drag

Didn’t seem to be an issue this latest quarter

Travel Retail and Asia Volatility

Weak conversion and volatile Chinese travel demand

Sluggish America Consumer and Category Mix

American growth flat and makeup is still slightly declining while the market is growing

So, Estée Lauder must defend premium pricing, reignite core brand growth, boost new brand performance and sustain China momentum, while preserving margin gains and navigating the economic headwinds ahead.

Amazon Q4 2025 Earnings

A classic MAG7 reaction this earnings season.

Report objectively strong revenue and earnings with a high capex budget, and then selloff after hours.

I would say Amazon’s Q4 2025 headline numbers were objectively strong:

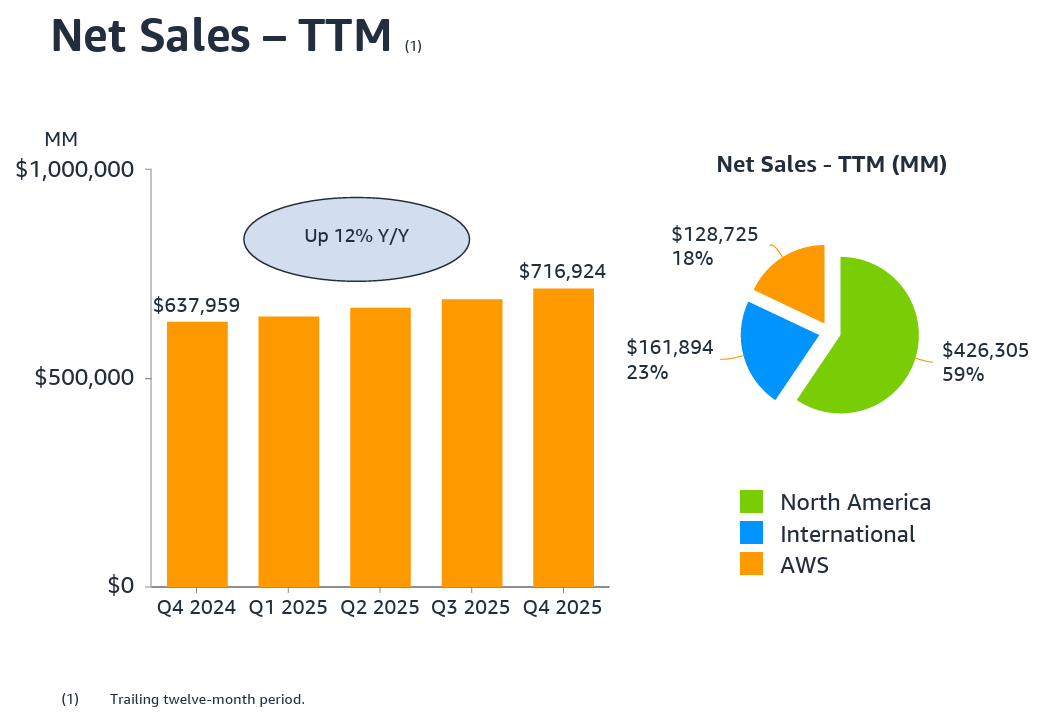

Net sales: $213.4B (+14% YoY) beating estimates of $211.5B

Earnings: EPS of $1.95, just a penny shy of the estimated $1.96

1. AWS (Cloud Computing)

AWS continues to outperform with revenue growth accelerating to 24%, its fastest rate in over three years. This was driven by GenAI services and their custom Trainium/Graviton silicon.

2. North America

The retail business remained highly efficient with operating margins improving to 9% (up from 8% last year). North America same-day delivery also saw a 30% increase in Prime member usage.

3. International

Revenue growth came in at 17%, although it was heavily bolstered by currency conversion rates. Operating profit dipped to $1.0B from $1.3B last year, as the business has been trying to cost cut to gain market share in emerging regions.

4. Advertising

This is not a reported segment, but definitely an important part of the business to mention. Advertising revenue reached $17.3B (+22% YoY), and Prime Video ads are now reaching an audience of 315M, which is providing a margin boost to the retail business.

Guidance came in at:

Amazon’s projected $200B of Capex came in sharply higher from an already massive $125B‑ish run‑rate.

Aaaannnnnd it spooked investors who thought the AI buildout would be a bit more gradual… causing Amazon to selloff 10%+ after hours.

For context, most of that spend is going into AWS infrastructure:

Data centers

Custom silicon (Trainium)

Networking gear

Low-orbit satellites

Robotics and logistics automation

Amazon is really leaning into the AI arms race, which has honestly surprised me.

Along with the increased Capex spend, Amazon has been laying off numerous corporate positions, totally around 30,000, with 14,000 last October and 16,000 this past January.

At the same time, it has over 1M robots in its fulfillment network with plans to automate hundreds of thousands of warehouse roles over the rest of the decade…

… investors are waiting patiently to see if the operating leverage will be realized here. I DO think this will take longer than the market expecting (maybe a year or two rather than a quarter or two).

There’s two different stories you can subscribe to here:

Bull Case: Capex pays off big, FCF explodes, AWS sustains 20%+ growth with expanding margins and robotics/AI investments deliver notable operating leverage, North America retail and ads compound at double-digits, and the International segment flips to high-teens growth

Bear Case: $200B Capex drags FCF negative through 2027–2028 without clear AI ROI, AWS decelerates amid hyperscaler competition, retail margins revert under consumer slowdowns and operating leverage disappoints

These are two extremes, but you essentially have to lean one way or another if you hold Amazon in your portfolio, or refuse to own shares.

I am going to subscriber to the former —> I own 250 shares of Amazon and will hold these shares confidently for years to come.

Disclaimer: The information provided in this publication is for informational and educational purposes only and does not constitute investment, financial, or other professional advice. ThePrivatePublicInvestor and its authors are not registered investment advisors or broker-dealers. All opinions expressed reflect personal views as of the date published and are subject to change without notice. While efforts are made to ensure accuracy, no guarantee of completeness or reliability is given. Past performance is not indicative of future results. The author may hold positions in securities discussed. Use of this content is at your own risk.

CAPEX

Nailed the capex position... The force pushing this is mighty but slow. It's gonna be a long light rain not a downpour. Positioning in the correct layers is the key to being in step with the capex rotation and the physics (water bucket). The ladder part of this year it will be copper and natural gas. Count on it.