How Cash Flow Fuels Growth

The Engine of Reinvestment and Scale

Cash flow is arguably the most important metric when evaluating the long-term sustainability of a business.

Cash flow determines may things along the growth curve of a company’s lifecycle.

It dictates whether a company can pay their day-to-day bills, survive economics downturns, maintain purchasing power, take on debt, and even hire the right talent within the organization.

Most investors understand that cash flow matters, but far fewer understand how cash flow, reinvestment opportunities and leverage work together to create some of the greatest wealth-generating businesses in history.

Cash flow can be the sole reason certain investors will turn away from an opportunity.

Let’s get into it.

Cash Flow Drives Equity Value

Free cash flow is the cash a business has left after covering its operating costs and the reinvestment needed to keep running — the cash actually available to the people who own it. The “take home pay”.

A share of stock is, at its core, a fractional ownership claim on the future cash flows of a business.

This is why finance theory dictates the intrinsic value of any asset is the sum of its future cash flows, discounted back to the present day (why people run DCF models).

You cannot pay dividends, buy back stock, fund M&A or pay off debt with net income. You can do all of those things with cash.

Earnings can be shaped in a dozen ways due to various accounting rules, but the cash a business actually generates is what ultimately sets the value of the equity, so for a growth company the central question is whether it produces consistent, growing cash flow.

Antonio Linares makes this point constantly:

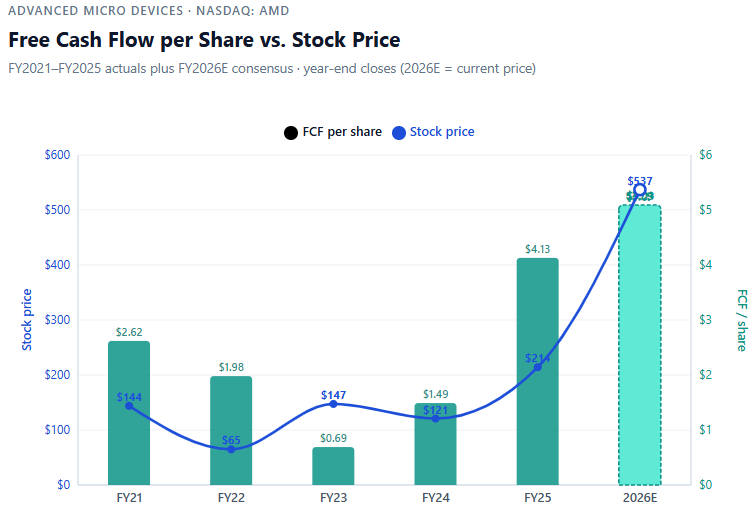

Over long periods of time, stock prices tend to follow free cash flow per share

While earnings can fluctuate due to accounting rules and timing differences, it is ultimately the cash generation power of a business that determines equity value (equity value = market cap).

The Cash Conversion Cycle Creates the Growth Flywheel

If cash is what ultimately sets the value of the equity, then how quickly a business turns its sales into cash matters just as much as how much cash it produces.

The faster a company collects cash and puts it back to work, the faster it can grow.

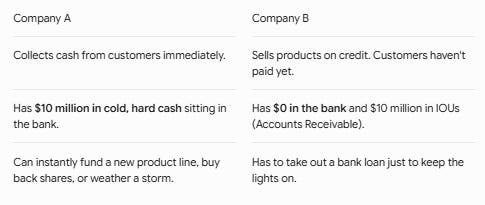

Take the below for example:

Company B has a huge lag time before it can collect cold, hard cash from its customers.

Company A can immediately invest that cash it collects back into the business.

That is the most important point here.

Company A has a faster cash conversion cycle (converting inventory or a service into cash), which allows the business to reinvest back into the business more quickly.

This stronger cash conversion cycle creates a powerful growth flywheel.

Businesses that convert earnings into cash more quickly can reinvest that capital sooner into high-return opportunities — whether that’s hiring salespeople, expanding capacity, entering new markets, acquiring customers or funding strategic initiatives.

The faster cash is generated and recycled back into the business, the faster the company can grow. That growth produces even more cash, which can then be reinvested into additional value-creating projects, creating a compounding effect over time.

In many ways, the cash conversion cycle is a key enabler of scale.

Companies that can efficiently turn revenue into cash have a structural advantage because they can fund growth internally, reduce reliance on external capital, and accelerate the pace at which they compound value.

Why Software Gets Premium Valuations

This dynamic is also one reason why software and other asset-light businesses often command higher valuation multiples than industries such as retail, apparel, distribution or manufacturing.

Because these businesses require relatively little incremental capital to grow, they can reinvest cash more quickly and earn higher returns on invested capital (ROIC).

In contrast, more capital-intensive businesses often have cash tied up in inventory, receivables, equipment and working capital, slowing the pace at which they can reinvest and compound growth.

Investors are often underwriting not a company’s current cash generation, but its future ability to convert revenue into cash at scale. Remember, markets are always forward looking.

This is particularly true in software, where the cost of serving each additional customer is often minimal once the product has been built. As a result, successful software businesses can scale rapidly without a proportional increase in capital requirements.

—> This combination of efficient cash conversion, low incremental costs, and attractive reinvestment opportunities creates one of the most powerful compounding engines in business.

It is also a major reason why venture capital has historically gravitated toward technology companies and why ecosystems such as Silicon Valley emerged around them — these businesses can reach scale faster, generate ROIC and create significantly more value from each dollar invested.

While a strong cash conversion cycle and ROIC create the foundation for growth, debt can accelerate this process even further when used responsibly.

Amplifying the Growth Flywheel with Debt

Debt is simply a tool that allows a business to invest more capital into attractive opportunities than it could using internally generated cash alone.

I personally view debt as accelerated capital allocation — a way for a great business to put more money to work today than its own cash flow alone would allow.

—> If management can borrow capital at a cost below the return generated by the business, that spread accrues to equity holders, amplifying returns on equity (ROE) and accelerating growth. So, if the return exceeds the interest payments, it’s a profitable decision, all else equal.

In this sense, debt acts as a multiplier on an already attractive business model.

The growth flywheel sequence:

Start with high-ROIC business.

Generate cash.

Debt adds more capital.

That capital gets invested at the same high ROIC.

ROE rises.

The key caveat is that debt only creates value when the borrowed capital is reinvested into initiatives that generate incremental cash flow at returns above the cost of borrowing.

Simply adding leverage to a business does not improve the economics but rather increases risk.

In fact, under-utilized debt can become a drag on performance by consuming cash flow through interest payments while producing no corresponding return!

BUT, for a cash-generative businesses, leverage can create a powerful growth engine:

The business generates cash, reinvests that cash at attractive returns, supplements those investments with low-cost debt (additional capital), and then uses the resulting increase in cash flow to further expand the business and repay lenders.

—> This dynamic is one of the primary reasons us evil private equity people utilize leverage in acquisitions!

It accelerates the value creation generated by a business with strong underlying economics, and returns capital to investors more quickly (I promise we aren’t evil… only sometimes).

Here is something that I have noticed in the private markets that plays out similarly in the public markets:

Debt imposes a degree of discipline on management teams.

The obligation to service interest payments forces scrutinized capital allocation decisions, reducing the temptation to pursue ‘pet’ projects, empire building, or other uses of capital that fail to maximize shareholder value.

When used prudently, debt encourages management to focus on initiatives that generate the highest returns on invested capital.

BUT.

If cash flows deteriorate or reinvestment opportunities fail to generate the expected returns, you are still obligated to pay back interest payments + principal.

In these situations, leverage can quickly destroy equity value… and, in extreme cases, transfer control of the business from shareholders to lenders (also known as Chapter 11 / bankruptcy).

Thus, debt is most effective when paired with businesses that generate durable cash flows, strong unit economics and a proven ability to reinvest capital at attractive rates of return.

Debt does not create a great business, but simply allows a great business to become great faster.

The Ultimate Compounding

The best businesses share a common set of traits:

Strong free cash flow generation

Efficient cash conversion

High ROIC

Long reinvestment runways

Prudent use of leverage

When these characteristics exist together, management can repeatedly turn every dollar of capital into multiple dollars of future value. Great for stocks!

Companies like Amazon are exceptional because they continuously convert capital into even more capital.

Ultimately, investors should focus less on reported earnings and more on how quickly a business turns earnings into cash, what returns it earns on that cash and how many opportunities it has to reinvest it.

Those factors are what drive sustainable growth and long-term value creation.

Disclaimer: The information provided in this publication is for informational and educational purposes only and does not constitute investment, financial, or other professional advice. ThePrivatePublicInvestor and its authors are not registered investment advisors or broker-dealers. All opinions expressed reflect personal views as of the date published and are subject to change without notice. While efforts are made to ensure accuracy, no guarantee of completeness or reliability is given. Past performance is not indicative of future results. The author may hold positions in securities discussed. Use of this content is at your own risk.

This is gold. It makes me realize that we can basically act like the CFO of our own lives. I try to treat my personal money exactly like a business: focusing 100% on cash flow to buy back my time and design the exact life I want.

Instead of trapping all my cash in things I can't touch, I want my money making immediate cash that I can instantly reuse—whether that's buying more assets or just funding my freedom.

Since keeping your money moving is the goal, do you think it's better to stick with traditional real estate for cash flow, or are you seeing better speed and flexibility in things like high-yield dividend funds today?