Turning Losers Into Tax Assets

A Practical Guide to Tax‑Loss Harvesting

“Tax efficiency is a valuable tool to enhance your overall financial plan, but it should complement, not dictate, your investment strategy.”

— Britannica Money

Tax‑loss harvesting sounds like something only hedge funds do.

In reality, it’s a vanilla tool almost every taxable investor should understand — especially in a year like 2025 where the index is up nicely but a long tail of stocks are bleeding red (consumer discretionary, real estate).

This is relevant today, as tax loss harvesting is prevalent mostly during Q4.

In this writeup, we’ll discuss what tax‑loss harvesting is, how the math actually works, why Q4 trading can get weird in single names, and which 2025 losers are showing classic tax‑loss selling footprints.

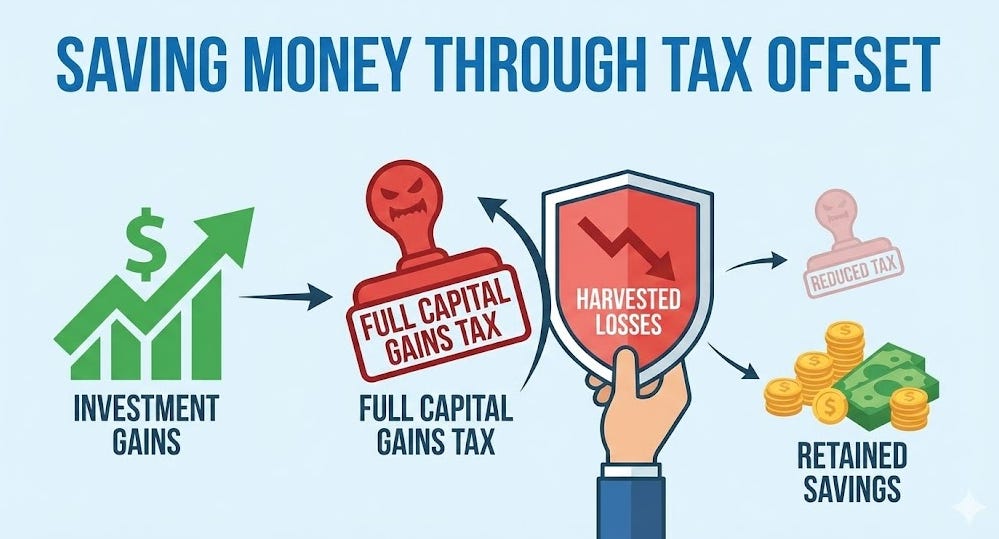

What Tax‑loss Harvesting Actually Is

At its core, tax‑loss harvesting is just this:

You sell an investment at a loss in a taxable account to realize that loss for tax purposes, and you use that realized loss to offset capital gains (up to $3,000 of ordinary income per year).

Key mechanics under current U.S. rules:

Losses net against gains first

Short‑term losses offset short‑term gains; long‑term losses offset long‑term gains. After that, any excess loss can be used against the other bucket.Then you can offset ordinary income up to $3,000 per year

If you still have net capital losses after offsetting all your gains, you can deduct up to $3,000 ($1,500 if married filing separately) against wages, business income, etc. Any unused amount carries forward indefinitely.The $3,000 limit is ancient and not indexed

That limit dates back to the 1970s and has never been inflation‑adjusted, so in real terms it has shrunk massively. That’s one under‑appreciated quirk: for high‑income investors, the real juice is almost always in offsetting capital gains, not in that tiny $3,000 ordinary‑income deduction.Losses carry forward forever

Any net loss you don’t use this year rolls forward to offset future gains and (again) up to $3,000 of ordinary income per year until it’s gone.

So the high‑level move is: turn “paper” losses into a tax asset, while keeping your portfolio risk where you want it.

The Wash‑sale Rule: The Trap Most People Vaguely Know, But Don’t Really Understand

The obvious hack would be: “Sell at a loss today, claim the deduction, buy the same thing back tomorrow.” That’s exactly what the wash‑sale rule blocks.

The IRS says your loss is disallowed if you buy the same or “substantially identical” security within a 61‑day window:

30 days before the sale…

…the day of sale…

…and 30 days after

The disallowed loss isn’t gone — it’s added to the cost basis of the new shares — but you don’t get to use it on this year’s taxes.

Two under‑discussed details:

The rule applies across accounts and across spouses. Buying the same stock in your IRA or your spouse’s account can still blow up the loss in your taxable account.

“Substantially identical” is fuzzier than people think. Two S&P 500 ETFs tracking the exact same index are risky territory; swapping from an individual stock to a broad sector ETF is usually fine.

The practical fix: if you harvest a loss, rotate into similar but not identical exposure (e.g., from one apparel stock into a peer, or from a single solar name into a clean‑energy ETF) and wait 31 days before rotating back if you want the original name.

Concrete 2025 Examples: How The Math Works

Consider a high‑income investor in 2025:

Realized $40,000 in long‑term gains earlier this year

AND is now sitting on ugly unrealized losses in a few names that have been hammered

Example 1: Rotating between beaten‑up consumer stocks (Nike and Starbucks)

Nike (NKE) and Starbucks (SBUX) have each dropped roughly ~10% YTD, making them prime tax‑loss harvesting candidates in the consumer space.

Suppose you:

Bought $30,000 of NKE earlier this year; it’s now worth $19,000 → $11,000 unrealized loss

Sell NKE today, realize that $11,000 loss, and immediately switch the proceeds into SBUX to keep your consumer exposure (not identical — different company, same sector).

On your 2025 tax return:

Your $40,000 gain is now reduced to $29,000 by the $11,000 loss

Assuming you’re in the 20% long‑term capital gains bracket, tax on that slice drops by about $2,200 this year

You still own a consumer name that could benefit if the sector recovers — you just traded which ticker you own while crystalizing the loss

REMEMBER: There is no limit to how much capital loss you can use to cancel out capital gains. If you have $1 million in gains and $1 million in losses, you can offset the entire amount!

Offsetting Ordinary Income: The $3,000 limit applies only if you have net losses left over after you have cancelled out all your capital gains (this should not be a goal, let’s hope your portfolio is doing better!)

Example 2: Taking a one‑two punch in consumer names

Lululemon (LULU), Deckers (DECK) and Freshpet (FRPT) are all down roughly 50–60% in 2025 and have been named multiple times in “tax‑loss selling” or “November effect” screens.

Imagine a taxable investor who:

Realized $20,000 in short‑term gains this year trading AI names

Is down $15,000 in LULU and $10,000 in FRPT

If they sell both losers before year‑end:

The $25,000 loss wipes out the $20,000 short‑term gain entirely

The remaining 45,000 net loss can offset $3,000 of ordinary income this year, with $2,000 carrying forward to future years.

At a top marginal ordinary rate, turning that $3,000 extra loss into an offset against wages is where a lot of the incremental benefit sits.

The kicker most people miss: this is mostly a timing game. You’ll usually pay tax later when you eventually sell the replacement position at a higher basis. The real value is:

Pushing taxes into the future (when your rate might be lower),

Converting high‑rate short‑term gains into lower‑rate long‑term gains,

And cleaning up dead money or a thesis you no longer believe in.

When Tax‑loss Harvesting Actually Happens — And How It Distorts Single‑stock Prices

Investors like to talk as if tax‑loss harvesting is a late‑December thing. In practice, there are layers:

Mutual funds and institutions often have October fiscal year‑ends, so a first wave of loss‑realization and window‑dressing hits in October, with a “November effect” bounce sometimes following when that pressure eases.

Retail and advisors tend to harvest in November and December, with many commentators explicitly calling the second half of November through mid‑December the peak tax‑loss window.

Academic work behind the January effect finds that stocks with bad prior‑year performance often see abnormal selling in November/December and a rebound in January as that pressure disappears.

A few important market‑structure implications:

Impact is highly single‑stock and small‑cap focused. The S&P 500 looks smooth (hypothetically, maybe not this year, lol) while individual losers — particularly less liquid or mid‑cap names — can get mechanically pushed lower into year‑end by tax‑motivated selling.

Tax‑loss selling can set up sharp January/February mean reversion. Once forced sellers are done, there’s often a vacuum on the offer side, and any incremental good news can trigger outsized rebounds — the classic “January effect” in prior‑year losers.

Robo‑advisors changed the seasonality at the margin. Many automated platforms now harvest losses throughout the year on small drawdowns, so some of the old‑school December seasonality has been dampened in broad indices, even if it still shows up in individual busted stories.

Takeaway for Q4: when you see an otherwise stable business down another 10–20% in late Q4 on no incremental news — tax‑loss selling is usually part of the story, not the whole story, but enough to move the stock.

2025 Stocks Caught in the Tax‑loss Harvesting Crosshairs

No one can say with certainty “this specific trade is tax‑loss selling.” But to conclude, here are some bigger names we believe have experienced tax-loss harvesting this year:

YTD Losses

Trade Desk (TTD): –66%

Deckers (DECK): –55%

Enphase (ENPH): –59%

Lulu Lemon (LULU): –51%

UnitedHealth Group (UNH): –36%

Target (TGT): –34%

Paypal (PYPL): –27%

Adobe (ADBE): –27%

Nike (NKE): –12%

Recommendation for Tax-loss Harvesting

Think about this strategy when you’ve already realized meaningful gains (especially short‑term gains taxed at higher rates) and are sitting on positions you no longer truly believe in.

In practice, it’s most powerful in Q4, when tax‑motivated selling is heaviest, single‑stock moves get distorted, and you can both clean up your portfolio and potentially set yourself up for a January/February rebound in prior‑year losers.

Disclaimer: The information provided in this publication is for informational and educational purposes only and does not constitute investment, financial, or other professional advice. ThePrivatePublicInvestor and its authors are not registered investment advisors or broker-dealers. All opinions expressed reflect personal views as of the date published and are subject to change without notice. While efforts are made to ensure accuracy, no guarantee of completeness or reliability is given. Past performance is not indicative of future results. The author may hold positions in securities discussed. Use of this content is at your own risk.

Do the new prediction market contacts with companies like Robinhood offer now play into this equation? Do you think retail investors can/will gamble their tax liability away?

Great write up! Very important for taxable investors indeed!